Symptom

Brokers were quoting off a feed everyone knows is messy.

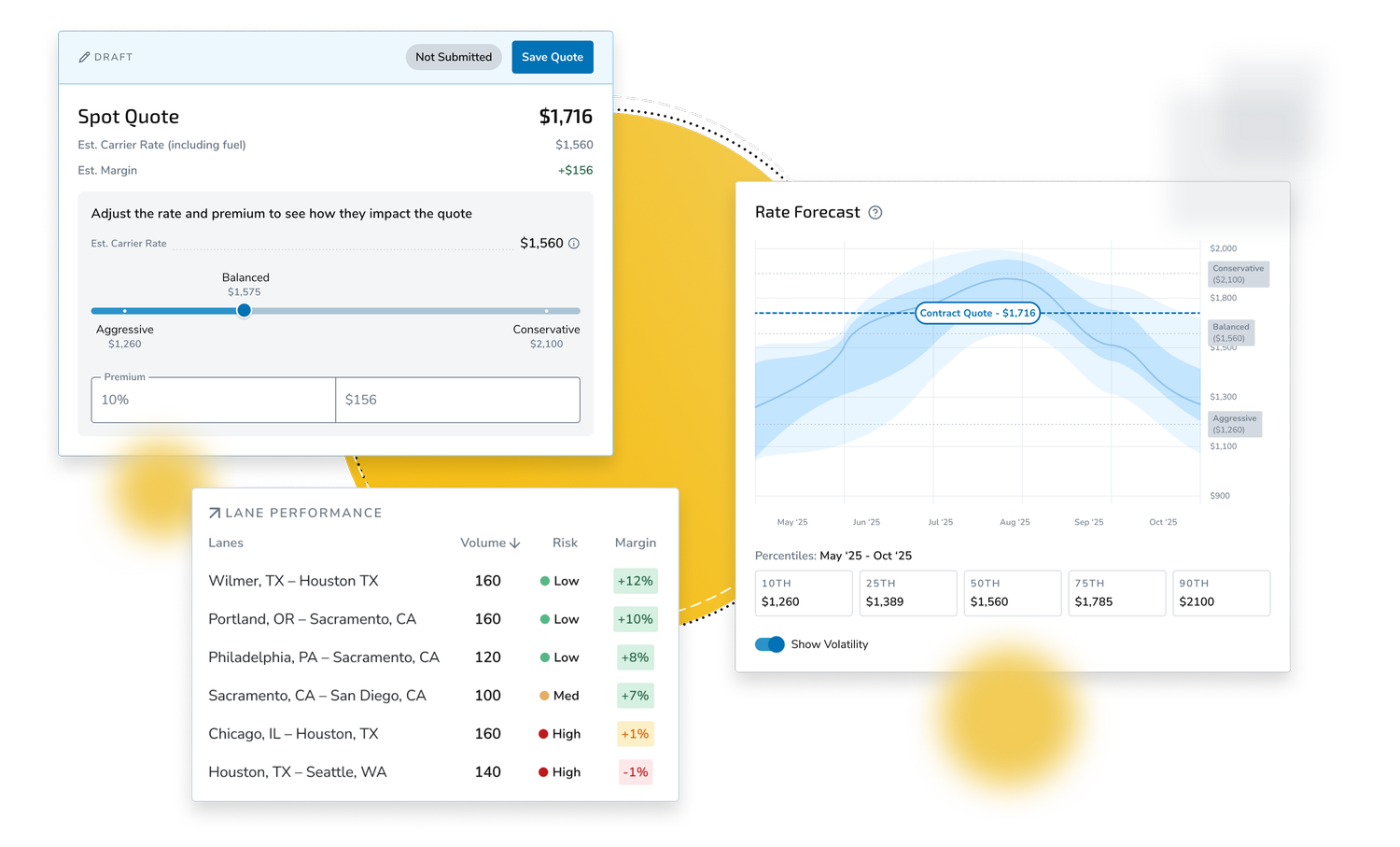

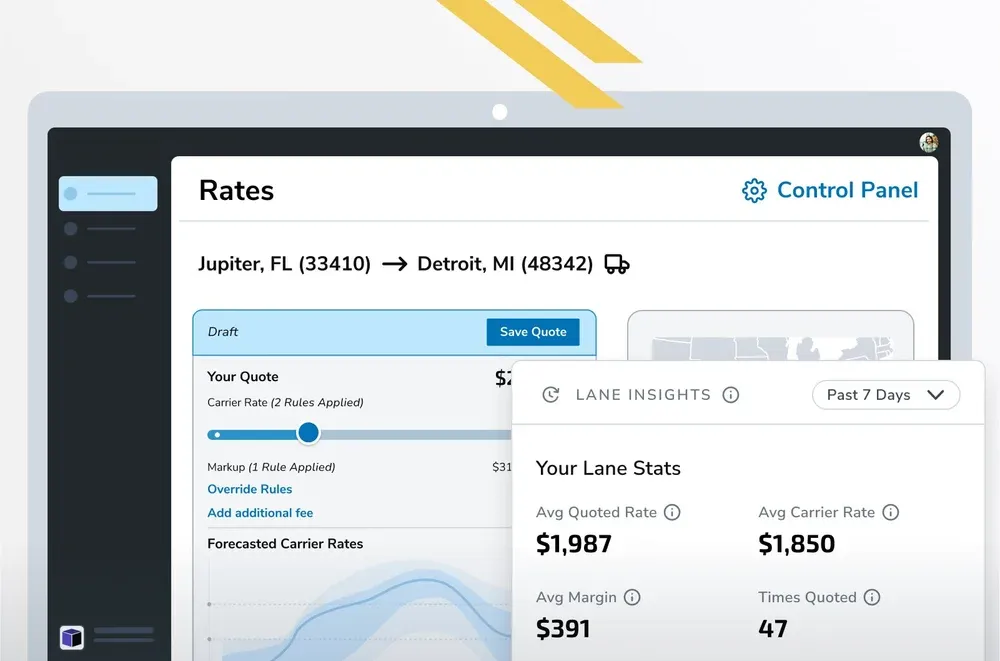

DAT is the leading rate feed in trucking. Everyone in the industry uses it. The problem is that DAT is peer-reported, which means it's noisy on its own: thin coverage on uncommon lanes, lagging signal on volatile ones, and rate bands wide enough to drive a truck through.

Genpro brokers were quoting off DAT directly, padded with intuition and recent memory. Rates came out inconsistent across the desk, slow on RFPs, and structurally exposed to whichever way the peer noise was leaning that week.